Regulatory changes for Crowdfunding: about the Regulation on European Crowdfunding Service Providers (ECSP) for Business

On November 10th 2020, the Regulation on European Crowdfunding Service Providers (ECSP) for business, which will be applicable as of November 10th 2021, entered into force. The present analysis of the upcoming changes highlights the future developments in crowdfunding/crowdlending but also some of the questions which will arise for all participants in the crowdfunding/crowdlending and

marketplace lending sector.

The Regulation on European Crowdfunding Services Providers targets crowdfunding services from crowdfunding platforms. Crowdfunding services, as defined in article 2 paragraph 1 letter a ECSP means the matching of business funding interests of investors and project owners through the use of a crowdfunding platform and which consists of the facilitation of granting of loans and the placing without a firm commitment basis. Letter d of the same article and paragraph defines a crowdfunding platform as a publicly accessible internet-based information system operated by a crowdfunding service provider.

With this new Regulation (ECSP), the European Union applies uniforming rules across the EU for the provision of investment-based and lending-based crowdfunding services related to business financing(1) as stated in above-mentioned article 2 ECSP. The biggest issue on an european level was perceived to be the lack of common rules and the sea of differing requirements that crowdfunding platforms had to adhere to depending on their country of origin. Therefore, one of the primary goals of the ECSP is to unify regulations across borders under one EU-wide regulation. Platforms can now apply for an EU passport. With this passport, crowdfunding platforms are able to provide their services within all EU countries and under a uniform set of rules which makes it easier to operate between the different countries.

According to the European Commission those new rules are expected to strengthen this relatively new form of finance, and provide advantages to companies which are seeking alternatives to bank financing. Additionally, there are some benefits for investors as well.

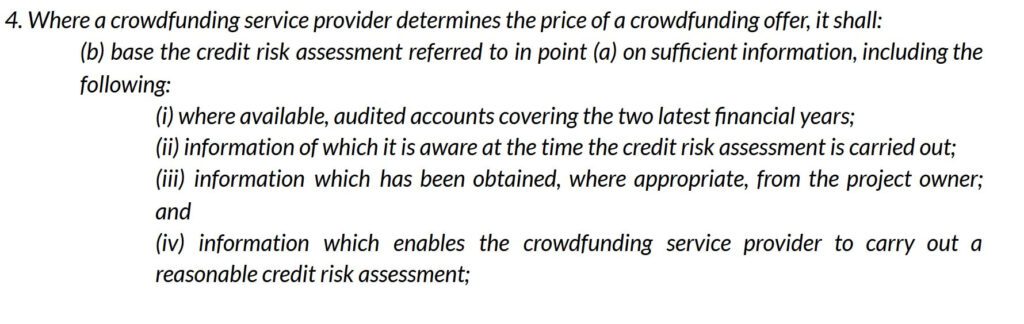

First, the rules on information disclosures for project owners and crowdfunding platforms among the countries are unified and therefore clearer. Second, there are now uniform rules on governance and risk management for crowdfunding platforms. This can be seen in various articles, such as in article 4, 12 and 20 ECSP. As to give an example of such rules: article 4 paragraph 4 letter b ECSP gives insight as to which criteria a crowdfunding provider shall base the credit risk assessment on.Fig. 2: Article 4 of the ECSP. Own illustration.

Last but not least, the supervisory powers of national authorities which oversee the functioning of crowdfunding platforms have been made stronger while simultaneously providing harmonization across the nations. However, there are some important articles which are worth a second look.

The Crowdfunding Regulation (“Regulation”)

As seen in article 1 paragraph 1 ECSP, “subject matter, scope and exemptions”, the Regulation lays down uniform requirements for the provision of crowdfunding services, for the organisation, authorisation and supervision of crowdfunding service providers. The uniform requirements are also for the operation of crowdfunding platforms as well as for transparency and marketing communications. Paragraph 2 shows a list with exemptions to the Regulation: those cases are (a) crowdfunding services that are provided to project owners that are consumers, (b) other services related to article 2 paragraph 1, letter a and c ECSP crowdfunding offers with a consideration of more than EUR 5 Mio. However, letter a arouses our attention:

The definition given in the Directive 2008/48/EC of the article 3 letter a, regarding what is considered a consumer reads as follows:

“ ‘consumer’ means a natural person who, in transactions covered by this Directive, is acting for purposes which are outside his trade, business or profession;”

Consequently, the Regulation does not apply to direct P2P loans, also known as direct consumer to consumer credit platforms. Therefore, the new Regulation applies only to crowdfunding services which are provided to non-consumers such as lending-based crowdfunding and equity-based crowdfunding. It only targets crowdfunding services to project owners inside trade, business or profession. Having said this, most European countries already have their own regulation when it comes to consumer financing/consumer loans.

To get more detailed information regarding the question “what happens in case a marketplace provides for business and consumer loans?”, we asked experts of the Financial and Capital Market Commission (FCMC), an autonomous public institution in Latvia. They were stating that for example in Latvia the issuing of loans to consumers is allowed only if a special licence from Consumer Rights Protection Centre is obtained. But those loans could be issued only using creditor’s own money, but not using funds attracted from investors. They further state, if those requirements are met, the provision of consumer and business loans could be combined in a single platform. However, since those products are completely different from each other each party should clearly understand which regulation is applied to the particular service.

In letter c of article 1 paragraph 2, there is an additional category which excludes crowdfunding offers from this Regulation with a consideration of more than EUR 5,000,000 over a period of 12 months. Such offerings potentially fall into another EU regulation and thus is exempted from the ECSP.

Addressed crowdfunding service providers

The question still remains “which crowdfunding service providers are addressed with the ECSP?” A closer look at article 3 ECSP gives valuable insights. article 3 paragraph 1 ECSP states:

“1. Crowdfunding services shall only be provided by legal persons that are established in the Union and that have been authorised as crowdfunding service providers in accordance with Article 12.”

In article 12 ECSP there are several criterias which a crowdfunding service provider needs to comply with in order to get the authorisation, such as general information about the company, descriptions of the prospective crowdfunding service provider, confirmations and various proofs a company needs to submit.

This poses the question of what exactly is meant by “established in the union”. Cases potentially exist where services are offered in countries of the Union but from a non-Union country. The Regulation does not mention how those entities are treated. However, the above-mentioned FCMC’s experts also elaborated on this topic: Since such crowdfunding service providers would target european investors and would offer loans in the EU as well, they too would fall under the crowdfunding regulation. So even those providers from outside the EU would have to be authorized by the EU in order for them to further carry out their services in the EU.

Paragraph 12 of the same article 12 offers companies which are already authorized in a EU member state, the simplification that they are exempted from having to resubmit documents or information that were already handed in previously.

Also interesting and especially essential to know for transnational service providers is article 18. It regulates the cross-border activity of crowdfunding services. The provider has thereby to submit, to the member state where the authorisation pursuant to article 12 was granted, a list with the member states, the service provider intends to provide crowdfunding services. Further requirements can be seen in article 18 paragraph 1 ECSP.

(Non) Fronting bank model

It is not yet entirely clear how the Regulation affects the fronting respectively non-bank model. Therefore, we have to take a closer look at the legal definition of a loan, as seen in article 2 paragraph 1 letter b ECSP:

“[...] (b) ‘loan’ means an agreement whereby an investor makes available to a project owner an agreed amount of money for an agreed period of time and whereby the project owner assumes an unconditional obligation to repay that amount to the investor, together with the accrued interest, in accordance with the instalment payment schedule [...]”

According to the Regulation, only those financings fall within the scope of application that must be unconditionally repaid. Qualified subordinated loans issued through a non-fronting bank model are not unconditionally repayable and are consequently excluded from the scope of the ECSP Regulation. Conversely, all loans issued on the fronting bank model however, are absolutely repayable and therefore fall under the new Regulation.

Mintos way

There is also another way to not fall under the new Regulation: The Regulation does not apply to investment platforms that possess an IBF or credit institution license. Just recently, mintos, a leading european marketplace for investing in loans, announced that they now have the permission to transform its business into a regulated financial investment marketplace. Therefore they get all the required licences from the Latvian regulator(2) and don’t fall under the new Regulation. It however remains to be seen whether other Marketplaces and/or Loan Originators will have the resources and/or will be willing to follow mintos’ example.

Summary & our view

Statement from the Head of Legal & Operations of i2 group Dominik Hertig: ”This Regulation certainly is a step into the right direction. We as customers and business partners of several crowdfunding platforms are confident that with the ECSP the potential of fraudulent actions can be reduced and investing through crowdfunding platforms will be more secure in the future. However, as discussed in this blog post, the crowdfunding regulation is novel and does not cover all open issues vis-à-vis crowdfunding (platforms). Also, and this happens with almost every new regulation, only time and experience will show how practical the rules and requirements set forth in the ECSP really are.”

With these recent developments having a professional partner that helps you navigate the legal landscape is more important than ever. i2 group can assist professional investors with our advisory services in any digital lending matter.

David Winistörfer, legal intern i2 group[1] This does not represent the official opinion of the Financial and Capital Market Commission (FCMC) but is the opinion of FCMC’s experts in response to our questions.

[2] https://ec.europa.eu/info/business-economy-euro/growth-and-investment/financing-investment/crowdfunding_en

[3] https://www.mintos.com/blog/mintos-obtains-european-investment-firm-license-to-become-the-go-to-investment-platform-for-retail-investors/

{kind=link}